Gen AI is probably the most important topics in technology development right now, enabling consumers and corporates to enhance their output as well as efficiency. From the investment perspective, one of the biggest debate right now is the ROI of the capital expenditure being spent on Gen AI.

Interestingly, a recent report from MIT actually shed some light on this topic. The report, titled “The Gen AI Divide: State of AI in Business 2025” (link), suggests that 95% of the enterprise spending on Gen AI are actually getting a 0% return right now. In other words, just 5% of integrated AI pilots are extracting millions in value, while the vast majority remain stuck with no measurable P&L impact.

If that is the case, much of the rapidly increasing spending on Gen AI might not even bear fruit (in terms of concrete P&L) impact, and that could mean trouble from the investment perspective. In order to assess whether the capex on Gen AI is reasonable or overly-optimistic, I collaborated with Co-pilot to perform a top down analysis:

- First we assume a 15% ROI on Gen AI capital expenditure would be a reasonable ROI hurdle,

- Second we calculated the resulted revenue uplift / cost reduction by multiplying the cumulative investment spend / capex spend between 2020 and 2030e by 15%

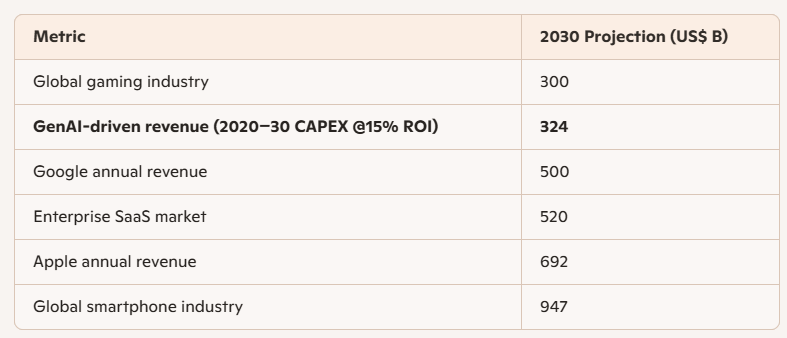

- Third we compare this number against the annual revenue generation by the mobile phone / gaming / SaaS industry as well as other estimates such as the estimated annual revenue of mega tech companies such as Google and Apple

- In the last step, based on such comparison, we try to make a high level on conclusion of whether this level of ROI (ie. 15%) is reasonable / achievable

Let’s see the result

Source: Copilot

According to Copilot,

“at $324 billion, GenAI‐driven revenue would just surpass the global gaming industry yet remain well below the revenues of enterprise SaaS, Google, Apple or the smartphone market. Hitting that level by 2030 implies GenAI must carve out a revenue stream on par with a top entertainment segment—entirely plausible given AI’s rapid adoption in sectors like media, healthcare, finance and manufacturing. However, this scale still trails broader tech markets, underscoring that while a $324 billion annual payoff is ambitious, it sits squarely within the realm of achievability if generative AI unlocks high-value, monetizable applications across multiple industries.”

So even though companies and corporate around the world are spending a huge amount of Gen AI, such amount of investment is still far from outrageous, and a healthy level of ROI still seem achievable on a high level.

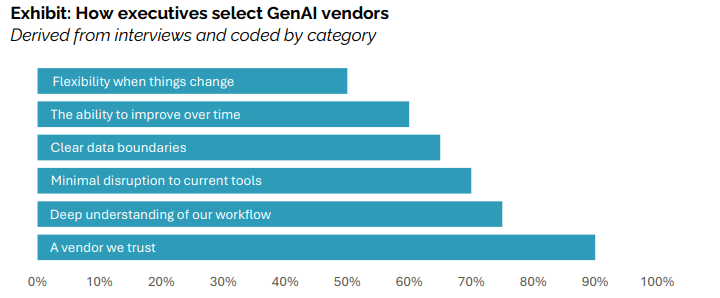

Going back to the MIT report, the report suggest a few criteria for GenAI vendors to be successful as well as a few tips for companies / corporates to successfully reap ROI from their Gen AI investment. For GenAI vendors to be successful, a strong relationship / trust with the client is still key; in additional, these vendor should have a deep understanding and smooth integration into the existing workflow of their client companies.

Source: MIT Nanda

In terms of how companies / corporates can successfully reap ROI from their Gen AI investment, the report suggests that these companies / corporates should:

- Demanded deep customization aligned to internal processes and data

- Benchmarked tools on operational outcomes, not model benchmarks

- Partnered through early-stage failures, treating deployment as co-evolution

- Sourced AI initiatives from frontline managers, not central labs

My final thought on this topic is that the Gen AI industry is indeed a rapidly evolving one, and A2A (Agent to Agent) network will be the next big thing within the industry. A2A network will shift AI agent from monolithic work to more collaborative work, while making Gen AI workflows more distributed. We will look more into the topic of AI agent in another post.

Leave a comment